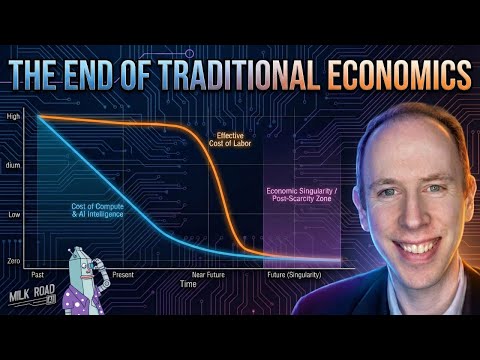

The Macro Shift: AI-driven hyperdeflation is colliding with the technical reality of autonomous AI agents creating their own crypto-backed economies, threatening a decoupling from human fiat systems.

The Tactical Edge: Investigate and build infrastructure that bridges human and AI economies, focusing on fiat-to-crypto rails that can accommodate agent-driven transactions to prevent a complete split.

The Bottom Line: The next 5-10 years will see an unprecedented economic transformation. Understanding AI's deflationary power and the emerging AI agent economy is critical for navigating a world where traditional economic models may no longer apply.

The time of practical AI agents is here, moving compute demand beyond pure GPU inference to a significant reliance on CPUs for coordination, data handling, and security.

Evaluate your agent deployment strategy now, prioritizing sandboxed environments (VPS, dedicated local servers) and exploring cost-optimized model routing to manage API expenses.

Prepare for a future where AI agents become integral to workflows, but recognize the hidden infrastructure costs and security implications, particularly the growing importance of CPU capacity and robust access controls.

The shift from "how" to "why" in AI agent capabilities creates a new, multi-trillion-dollar market for companies that can capture institutional decision logic.

Invest in or build agentic systems that are in the "right path" of business processes, actively capturing decision traces from unstructured data.

Hundreds of context graphs will be in production at scale within a year, defining a new "context graph stack." The winning companies will be those that master this flywheel, extracting value to accelerate automation and build deep, defensible moats.

The shift from linear, bottleneck-driven technological progress to a multi-layered, interconnected advancement model in AI has rendered traditional forecasting obsolete, forcing a re-evaluation of what "singularity" truly represents.

Prioritize adaptability: Invest in modular, composable AI infrastructure and tools that thrive in multi-layered, unpredictable environments, rather than betting on single-bottleneck solutions.

The inability to narrate AI's future means traditional roadmaps are obsolete; success hinges on navigating simultaneous, interconnected advancements and embracing the emergent.

The era of infrastructure-heavy tech deployment is over; AI's internet-native nature means immediate, widespread application. This shifts the competitive advantage from capital-intensive builds to rapid iteration and data leverage.

Invest in companies that are not just using AI, but are fundamentally rethinking their business models around AI's ability to collapse traditional cost structures and accelerate product development.

AI is a force multiplier for both individual opportunity and national power. Understanding its immediate deployability and the new rules of company building is crucial for investors and builders aiming to lead in the next wave of innovation over the next 12-24 months.

Unprecedented fiscal and monetary stimulus, coupled with a deregulatory environment, creates a powerful tailwind for financial assets and tech, driving a capital investment super cycle.

Investors should prioritize companies with proprietary data and GPU access, as these are the new moats in an AI-driven world where traditional software leads are eroding.

The convergence of a stimulative macro environment and AI's disruptive force means capital will flow to those who can scale, innovate, and navigate complex policy landscapes, making strategic positioning now critical for future relevance.

The macro trend of autonomous AI agents is shifting compute demand beyond GPUs, creating an unexpected CPU crunch and forcing a re-evaluation of on-premise inference and cost-optimized model routing for security and efficiency.

Investigate hybrid compute strategies, combining secure local environments (Mac Minis, home servers) with cloud-based LLMs, and explore multi-model API gateways like OpenRouter to optimize agent costs and performance.

AI agents are here, demanding a rethink of your compute stack and security protocols. Prepare for a future where CPU capacity, not just GPU, becomes a critical bottleneck, and strategic cost management for diverse AI models is non-negotiable for competitive advantage.

The move from general-purpose LLMs to specialized AI agents demands a new data architecture that captures the *why* of decisions, not just the *what*. This creates a new, defensible layer of institutional memory, moving value from raw model IP to proprietary decision intelligence.

Invest in or build agentic systems that are in the *orchestration path* of specific business processes. This allows for the organic capture of decision traces, forming a proprietary context graph that incumbents cannot easily replicate.

Over the next 12 months, the ability to build and extract value from context graphs will define the winners in the enterprise AI space, creating a new "context graph stack" that will be 10x more valuable than the modern data stack.

Survive, Then Thrive. After massive liquidations, the strongest assets and narratives (e.g., privacy plays like Zcash) recover first. Focus capital on names showing relative strength post-wipeout, as they are the first to capture returning liquidity.

Revenue is the New Narrative. The game has changed. The market now demands clear revenue streams and legal structures that align token holders with protocol success. Valueless governance tokens are out; tokens tied to real business operations are in.

On-Chain TradFi is Here. Platforms like Hyperliquid are successfully bringing assets like the NASDAQ on-chain, proving crypto-native demand for traditional markets. This represents a major new frontier for DeFi protocols looking to capture volume.

**Fiscal is the new Fed.** Government spending, not central bank policy, is the dominant force in the economy. Stop looking for a traditional recession; the deficit is the stimulus that won’t quit.

**The Fed is re-opening the liquidity spigot.** The era of Quantitative Tightening is over. A gradual but persistent expansion of the Fed's balance sheet is coming, which will provide a tailwind for assets.

**Own scarce assets.** The long-term debasement of fiat currency is the default path. Alden remains constructive on Bitcoin, viewing its current phase as a prelude to a significant move higher in the coming years.

Security Is No Longer an Afterthought: The Crucible Wallet’s native Ledger integration provides the first hardware-secured, consumer-friendly way to manage TAO and subnet tokens, addressing a major security gap in the ecosystem.

Automated Strategy Beats Day Trading: The "Staking to Core Alpha" feature offers a powerful tool that automatically reinvests yield into a customizable portfolio of subnets, saving users from the overwhelming task of constantly researching and reallocating assets.

Capital Flow is King: The wallet's primary mission is to redirect staked TAO from the root network into deserving subnets, providing them with the capital needed to grow and achieve commercial success, which in turn strengthens the entire Bittensor network.

The Real Metric Is GDP, Not Volume. A million dollars in daily card spending on real-world goods is a far more powerful signal of adoption than hundreds of millions in AMM swap volume. Watch the growth in real economic activity, not just on-chain shuffling.

Infrastructure Is the Bottleneck. The race isn't just to launch another neobank; it's to build the underlying pipes. Protocols like Frax that power multiple stablecoins and neobanks are positioned to capture value from the entire ecosystem's growth.

The End Game Is a Parallel Financial System. Crypto neobanks are the final link needed to close the economic loop. They enable a world where a user can save, earn yield, and spend entirely on-chain, making the concept of a bank account obsolete.

Verticalize or Die. Protocols are aggressively bundling services to capture value and own the user experience. Standalone products are at risk of being outcompeted or acquired cheaply, as seen with Pump's acquisition of Padre.

The Middle-Ground ICO is Hot. Highly anticipated projects like MegaETH are finding success with public sales that sit between illiquid private rounds and expensive public listings. For investors with capital, these offer a compelling risk/reward profile.

Performance Trumps Purity. The debate is shifting. While credible neutrality is a good marketing angle, the rise of high-performance chains like Hyperliquid suggests users and capital will flow to the best product, regardless of its decentralization score.

Every App is a Future Fintech: Major applications will become their own central banks, issuing native stablecoins to control their financial rails, capture yield, and eliminate the platform risk inherent in relying on third-party issuers.

Infrastructure, Not Brands, is the Real Game: The battle isn't over which stablecoin brand wins, but who builds the underlying rails that make a fragmented ecosystem of thousands of dollars feel like one seamless, interoperable network.

The Stablecoin Market is Just Getting Started: Today's ~$300 billion stablecoin float is a "ridiculously small number." Expect a 100x expansion as money migrates from legacy bank ledgers to programmable, on-chain infrastructure.